If your organization manages a corporate art collection, you’ve likely faced questions about how to justify, document, and potentially leverage that collection financially. What was once considered a static cultural amenity is increasingly recognized as a strategic asset—one that can provide liquidity without disrupting operations or diluting ownership. This guide walks you through the fundamentals of art financing for corporate collections and shows you how disciplined collection management makes it all possible. None of this scales without proper asset inventory management underneath. Some firms treat select pieces as investment art in their own right. Pulling these threads together is the essence of art management.

Table of Contents

What Is Art Financing and How Do Art Loans Work?

Risks and Challenges in Art Lending

Building a Strong Foundation: Collection Data and Documentation

How Onward Supports Art Financing Workflows

Best Practices for Responsible Art Lending

Getting Started With Art Finance Using Onward

Art Financing FAQ

Art Finance at a Glance

Art finance, also known as art-backed lending, allows collectors to use their artworks as collateral to secure loans, enabling them to access liquidity without selling their pieces. For corporate collections, this means treating fine art not just as decor or cultural investment, but as a balance-sheet asset that can support treasury objectives.

Art lending refers to the process of pledging artworks to lenders—private banks, financial institutions, auction houses, or specialist firms—in exchange for credit facilities. The works typically remain in your possession, displayed on office walls or campuses, secured through legal agreements, insurance endorsements, and periodic inspections. Organizations in New York, London, Hong Kong, and Zurich increasingly treat art as a strategic asset class similar to real estate or private equity.

- Unlock tens of millions in capital for strategic initiatives

- Retain full ownership and cultural impact of key works

- Support business growth through flexible, non-dilutive financing

- Maintain operational continuity—works stay on display

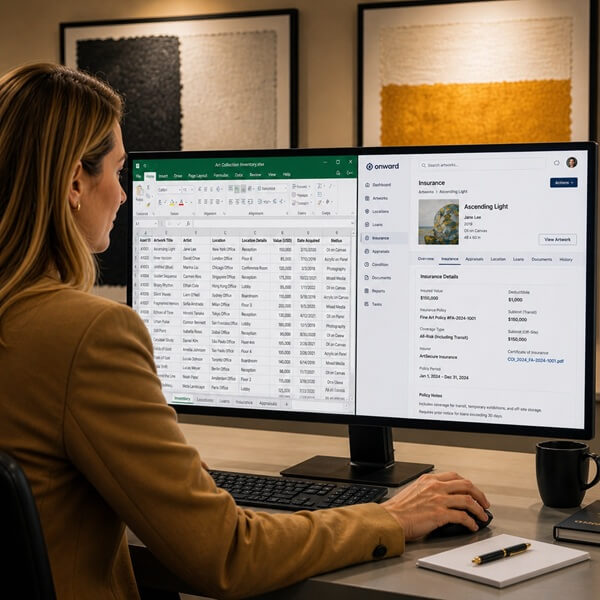

Art Onward is the software layer that helps you track, document, and optimize your collection so you can safely engage with lenders. By centralizing inventory, provenance, conditions, and valuations in a lender-ready format, Onward streamlines due diligence that traditional spreadsheets cannot match.

The Modern Art Market and Corporate Collections

The global art market reached $65 billion in sales in 2022 according to UBS and Art Basel reports, with blue-chip segments rebounding to contemporary art up 12% year-over-year by 2025. Corporations, universities, and healthcare systems have accumulated substantial fine art collections over decades—Bank of America’s global art program holds over 30,000 works, and JPMorgan’s collection exceeds 40,000 pieces built since the 1950s. (see Art Basel Art Market Report)

These collections now sit at the intersection of culture, branding, ESG initiatives, and balance-sheet management. A single work by artists such as Yayoi Kusama, Gerhard Richter, or Kerry James Marshall can represent $5–20 million in concentrated value, demanding treasury oversight for impairment testing and fair value accounting.

Art financing has become more accessible in recent years, with a broader ecosystem of banks and specialist lenders now providing art loans and art lending programs. This environment increases opportunity but also raises the operational burden on you to maintain accurate inventory, provenance, condition, and valuation data.

Accurate art valuation is the foundation of any financing arrangement — lenders require independent appraisals before extending credit.

Financial institutions that hold art collections as part of their corporate identity or client-facing spaces face these challenges at scale, making structured collection management — supported by a dedicated art collection app — essential.

What Is Art Financing and How Do Art Loans Work?

Fine art financing strategies typically use art as collateral for credit facilities—term loans, revolving credit lines, or advances against sale—without transferring ownership. The borrower retains the works while the lender holds a secured interest.

The process begins with third-party appraisal of artworks, typically using low auction estimate methodology. Lenders then establish loan-to-value ratios, conservatively set at 40–60% of appraised fair market value to account for art’s illiquidity—meaning a £1 million painting could secure a loan of approximately £500,000. Loan terms typically range from one to five years, with interest rates at SOFR plus a 2–5% spread. Collateral is secured through UCC filings, bailee letters, and lender-as-additional-insured endorsements on insurance policies.

| Provider Type | Typical Loan Range | Key Characteristics |

|---|---|---|

| Private banks (JPMorgan, Merrill Lynch) | $10M+ | Integrated with wealth/treasury services |

| Major auction houses (Christie’s, Sotheby’s) | $1M–$250M | Fast closes, deep market expertise |

| Specialist lenders (Athena Art Finance) | Varies | Broader access, potentially higher rates |

Eligibility typically requires museum-quality pieces, ironclad provenance, clear legal title, and documented secondary market liquidity. An advance against sale suits pre-consignment liquidity, where auction houses advance 50–70% of the low estimate before sale. A hold-and-pledge structure fits ongoing credit facilities where art remains on-site with periodic inspections. Your ability to produce complete, accurate documentation from a system like Onward can significantly accelerate lender due diligence and improve your negotiating leverage.

Organizations should also confirm their art collection insurance reflects current market values when pledging works as collateral.

Why Organizations Use Art Finance: Strategic Use Cases

Art finance functions as a treasury and strategy tool, not a last-resort cash source. Common use cases include:

- Real estate projects: Bridging capital for office renovations or campus expansions while mortgage financing is finalized

- Capital campaigns: Supporting museum, performing arts, or educational facilities without liquidating anchor works

- Technology upgrades: Funding analytics platforms, infrastructure, or digital transformation initiatives

- Collection growth: Acquiring key pieces that complete collection themes, repaying when other assets are sold

- ESG/DEI initiatives: Financing acquisitions of underrepresented artists to strengthen diversity goals

Consider a New York-based financial institution using part of its fine art collection to secure a credit line while renovating client floors. By pledging a $15 million subset of works during a $50 million office renovation, the firm maintains liquidity without removing all artwork from public areas—rotating unpledged pieces to sustain visual impact. Responsible art financing requires rigorous risk management, clear internal policies, and cross-functional collaboration between finance, legal, and art program leadership.

Risks and Challenges in Art Lending

Art lending carries reputational, legal, and financial risks if not managed carefully. The high-profile Annie Leibovitz case in New York illustrates the dangers: in 2009, an $8 million loan against her photography archive defaulted amid a market crash. Aggressive loan-to-value ratios and documentation gaps led to seizure threats and media scrutiny.

Key risk categories include valuation risk (art fell 25% in 2008–09 and remains volatile), provenance and title gaps (missing documentation can reduce loan-to-value by 20–30%), condition issues, security concerns for works spread across dozens of offices, market liquidity risks for niche artists, and regulatory compliance (KYC/AML requirements for international works).

Verified art provenance strengthens a lender’s confidence in the asset and can improve loan terms.

Corporate collections face amplified challenges: works scattered across 50+ offices, incomplete records from legacy acquisitions, missing invoices, and undocumented internal moves. A platform like Onward helps you mitigate these risks by systematizing data, documentation, and location/condition tracking before you approach a lender.

Building a Strong Foundation: Collection Data and Documentation

Preparing your collection for art finance starts with comprehensive data. Every lender will expect documentation covering: artist, title, date, medium, and dimensions (standardized per AAA guidelines); acquisition details including date, price, and invoice or donation agreement; current valuation with annual appraisals cross-checked with Artnet and auction comparables; location history with internal moves logged; and condition reports with high-resolution photos and conservation notes.

Provenance is paramount. Chains of ownership from creation—via bills of sale, exhibition histories, export licenses—must be intact. Gaps can slash loan-to-value by 20–30% or disqualify works entirely. Onward centralizes this information by digitizing documents, linking them to individual objects, and maintaining version-controlled records accessible to finance, legal, and curatorial teams. Organizations using Onward can quickly export lender-ready inventories and document packets, reducing the initial review and documentation stages from months to weeks.

How Onward Supports Art Financing Workflows

Onward is a B2B SaaS platform designed specifically for enterprise art collection management. It does not provide loans itself but enables safer, more efficient collaboration with art finance providers.

A robust collection management platform helps track which works are pledged, on loan, or available. The right art management software centralizes all of this in one searchable system.

| Feature | How It Supports Art Financing |

|---|---|

| Centralized catalog | Standardized fields, custom attributes (pledged status, lien info) |

| Loan tracking | Tag objects as collateral, record terms, maturity dates, LTV ratios |

| Provenance vault | Secure storage for title evidence, import/export paperwork |

| Insurance management | Track policy numbers, coverage limits, lenders as additional insured |

| Analytics dashboards | Total insured value, pledged vs. unencumbered works, concentration risk |

Audit trails ensure GAAP compliance, while integrations with appraisers streamline valuation updates. For a multinational law firm unifying New York and London collection data, or a healthcare system tracking works across dozens of clinics, Onward provides the foundation for confident lender engagement.

Integrating Art Finance Into Broader Financial and Collection Strategy

Treat art finance as part of a coordinated strategy covering risk, accounting, and collection development—not as ad hoc borrowing. Corporate finance teams can map art assets into existing asset registers and risk frameworks, including fair value reporting under ASC 820, impairment testing, and internal controls. Collection policies should explicitly address when and how art may be used as collateral, approval thresholds, and any ethical or reputational boundaries—for example, excluding culturally significant works from pledging.

Onward serves as a bridge between art program leadership and finance by providing common, audit-ready data and reports in formats finance teams understand. Balance liquidity needs with mission by setting internal guidelines on which categories of works are eligible for art lending. Periodic portfolio reviews using Onward—at least annually—allow you to reassess valuations, collection value and appreciation, and overall collection health within conservative risk limits.

Best Practices for Responsible Art Lending

- Establish cross-functional governance: Form an internal committee including finance, legal, risk, facilities, and art program leadership to evaluate any proposed art finance transactions.

- Secure independent valuations: Obtain third-party appraisals from recognized firms and cross-check them with external art market data and Onward’s collection analytics.

- Maintain documentation discipline: Log all loan covenants, reporting requirements, lender inspections, and insurance obligations directly in Onward. Review them quarterly.

- Pilot before scaling: Start with a small, well-documented transaction ($2–5 million) before committing larger portions of your collection, especially if operating across multiple jurisdictions.

- Communicate clearly: Inform internal stakeholders about which works are pledged, where they can be displayed, and what constraints apply during the loan term. Transparency prevents operational surprises.

Case Scenarios: From Static Asset to Strategic Tool

Multinational Law Firm: A law firm with offices in New York and London held a $25 million collection across both locations but lacked unified records. After migrating to Onward and consolidating provenance documentation, the firm identified a $7 million subset eligible for pledging. A Christie’s Art Finance facility closed in 45 days, funding a client center renovation while signature works remained on view.

Healthcare System Expansion: A regional healthcare system tracked over 1,000 pieces across hospitals and clinics using Onward’s location and condition monitoring. When capital was needed for facility expansions, the system secured a $10 million credit line against diversified holdings. Lender inspections proceeded smoothly because condition reports and photos were current and accessible.

DEI-Focused Acquisitions: A financial services firm sought to improve diversity representation in its collection. Using art finance, it funded acquisitions of works by underrepresented artists, aligning capital strategy with cultural and ESG goals. Loan repayment was structured against future deaccessions, managed through Onward’s loan tracking module.

Getting Started With Art Finance Using Onward

- Audit current data: Assess what records exist, where gaps lie, and which works carry the highest value.

- Consolidate in Onward: Migrate records, standardize taxonomy, and digitize provenance documents (typically 2–4 weeks for enterprises).

- Identify high-value subsets: Flag works with strong secondary market presence and clean title.

- Engage trusted advisors: Connect with banks, auction houses, or specialist lenders who match your scale and needs.

- Define internal policies: Establish approval thresholds, eligible work categories, and reporting requirements.

Even if you’re not yet certain you’ll pursue fine art financing, strengthening control over inventory, loans, documentation, and analytics positions you for future opportunities. Ready to transform static assets into strategic tools? Contact us at artonward.com/contact-us to see how disciplined collection management supports both culture and long-term financial resilience.

Art Financing FAQ

What is art financing?

Art financing allows collectors and organizations to borrow money using artwork as collateral. Lenders assess the art’s market value, provenance, and condition to determine loan terms, giving borrowers access to liquidity without selling their collection.

How does art-secured lending work?

A lender appraises the artwork, typically lending 50% to 70% of its fair market value. The art may remain on display or be held in a secure facility during the loan term. Interest rates and terms vary by lender, loan size, and the quality of the collateral.

What types of art can be used as collateral?

Paintings, sculptures, photographs, and prints by established artists with strong auction records are most commonly accepted. Lenders favor works with clear provenance, recent appraisals, and active secondary markets. Emerging or decorative art is harder to finance due to valuation uncertainty.

What are the risks of art financing?

Key risks include market depreciation that reduces the collateral’s value, the cost of storage and insurance during the loan term, and the possibility of forced sale if the borrower defaults. Accurate and current valuations are essential to managing these risks effectively.

Who provides art financing services?

Specialist art lenders, private banks with art advisory divisions, and some auction houses offer art-secured loans. Each has different minimum loan thresholds, interest rates, and collateral requirements. Corporate borrowers typically work with banks that understand institutional collection structures.

Do I need an appraisal before applying for art financing?

Yes. Lenders require an independent appraisal from a qualified appraiser — typically someone accredited by ASA or AAA. The appraisal must reflect current fair market value and include provenance verification, condition assessment, and comparable sales data.